Do I Still Owe the Bank After a Mortgage Foreclosure?

Upsolve is a nonprofit that helps you eliminate your debt with our free bankruptcy filing tool. Think TurboTax for bankruptcy. You could be debt-free in as little as 4 months. Featured in Forbes 4x and funded by institutions like Harvard University — so we’ll never ask you for a credit card. See if you qualify →

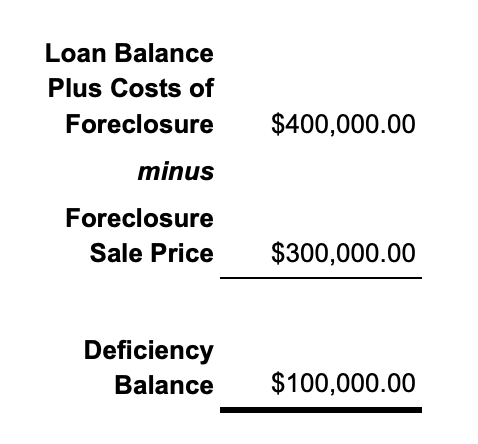

The proceeds of a foreclosure sale don't always cover the total balance that a homeowner owes their lenders. When this occurs, the remainder owed is referred to as a deficiency balance. State law dictates when and how a lender may hold a borrower responsible for a deficiency balance. Borrowers may proactively work out a repayment arrangement with their lenders, they may seek to have the balance forgiven via bankruptcy, or they may be held responsible for repayment of the balance via a deficiency judgment.

Written by Lawyer John Coble. Legally reviewed by Jonathan Petts

Updated October 13, 2025

Foreclosure hurts homeowners. If your home is foreclosed on, the lender will sell it and you’ll have to find a new place to live. If the sale proceeds don’t cover what you owed on your mortgage, the lender may go after you for the difference. This is called a deficiency. This article discusses why creditors sue for deficiencies after a mortgage foreclosure along with how to use state and federal laws to prevent having to pay this extra money.

What Is a Deficiency Balance?

If your foreclosed home sells for less than what's needed to pay off the mortgage and the costs of the mortgage foreclosure, you have a deficiency balance. The calculation is pretty simple:

The mortgage lender may choose to sue you to get a judgment to collect this deficiency balance. Until the foreclosure crisis of 2008-2010, it was rare for lenders to sue for the deficiency balance because the prices of real property were increasing. This changed when real estate values fell.

How Do Creditors Collect Deficiency Judgments?

When you take out a mortgage loan, you sign a promissory note. This is your promise to make your mortgage payments. You also sign a mortgage or deed of trust, which makes the home the collateral for the loan. Before the foreclosure process, your mortgage debt is a secured debt because your home “secures” the loan as collateral. During the foreclosure process, the servicer takes the collateral and sells it.

If there's a deficiency balance, this is called an unsecured debt since the collateral isn’t there to back it up anymore. The mortgage is gone, but the promissory note remains. Secured debts and unsecured debts are treated a little differently, which is why this distinction matters. For instance, unsecured debts can be discharged in bankruptcy.

If the lender wins a deficiency judgment against you, it can collect by garnishing your wages, levying your bank accounts, and/or seizing your assets. The lender may also place a lien on your property. A judgment lien is a special type of secured debt that can attach to all your property or real estate. If there's non-exempt equity in your property for the lien to attach to your deficiency debt will become secured again. This will matter if you file bankruptcy, which we’ll discuss later.

State Laws Concerning Deficiency Judgments Vary

Some states require lenders to go through the courts to foreclose. When a lender brings a foreclosure action as a lawsuit this is called a judicial foreclosure. In other states, lenders can choose to do a judicial foreclosure or a nonjudicial foreclosure. A nonjudicial foreclosure doesn't require a judge. The mortgage company or the foreclosure trustee simply follows the state's laws for holding a foreclosure sale.

State laws covering deficiency judgments vary from state to state. Most states allow deficiency judgments, but there are often restrictions. For example, some states forbid suing for deficiency judgments if your primary residence was foreclosed on. Other states only allow deficiency judgments if the claim is brought as part of a judicial foreclosure.

Sometimes, the loan contract rather than state law forbids a deficiency judgment. A loan that doesn't allow a deficiency balance is called a non-recourse loan. With non-recourse loans, the lender can only recover the collateral. Loans that allow deficiency judgments are called recourse loans.

Also, even if the lender can sue you, they may choose not to because lawsuits are expensive and time-consuming. If your lender doesn’t think you have a way to pay the judgment, they may not want to pursue the deficiency judgment. Also if the balance isn’t very high, it may not be worth suing.

State Laws Often Limit How Much a Deficiency Judgment Can Be

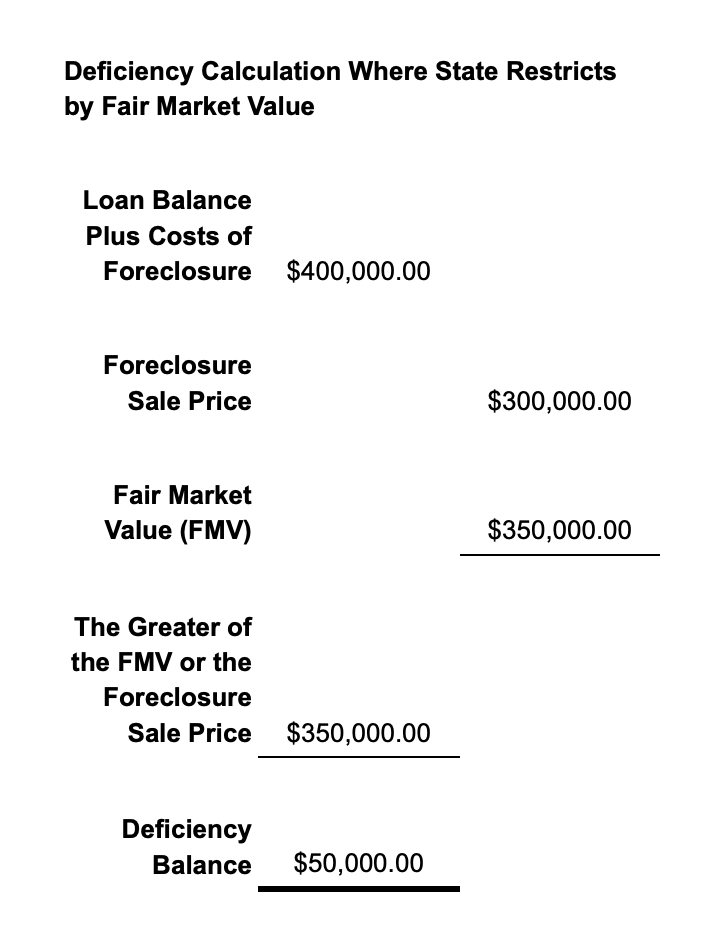

Many states limit the maximum deficiency amount the lender can collect. They do this by calculating the deficiency using the fair market value (FMV) of the foreclosed property rather than the foreclosure sale price. If the home sells for less than the fair market value, the deficiency will be calculated using the fair market value. If the home sells for more than the fair market value, the sale price will be used instead. This works in the borrower’s favor. Consider the example below:

In this example, the loan balance is $400,000, the foreclosure sale price is $300,000, and the fair market value is $350,000. The home sold for less than the fair market value. If you’re in a state with a fair market value restriction, you’ll only owe $50,000 ($400,000 - $350,000).

How To Defend Yourself Against a Deficiency Claim

In some states, the lender must file a judicial foreclosure to get a deficiency judgment. Other states require lenders to bring a separate lawsuit for a deficiency judgment. Whichever way a deficiency claim is brought, you may have legal defenses that prevent the lender from getting the judgment or reduce the judgment amount.

If robo-signed documents were used in your foreclosure, you can bring this as a defense to stop the foreclosure and have the deficiency eliminated. Robo-singing was common during the foreclosure crisis in 2008. Robo-signed documents may have been forged, signed by low-wage employees who didn't understand what they were signing, or signed by people using false job titles.

You may be able to stop or limit a deficiency judgment by using your state’s laws. As mentioned before, some states set a maximum deficiency amount based on the fair market value of the home. In other states, lenders can’t pursue a deficiency judgment if the home they foreclosed on is your principal residence. Many states also have very short statutes of limitations. This is the timeline the lender has to bring a deficiency lawsuit. If the lender brings the deficiency suit after the statute of limitation has passed, you can use this as a defense.

You may be able to negotiate to lower or eliminate a deficiency judgment if you act before the foreclosure. You can do this by using a short sale or a deed in lieu of foreclosure. A short sale is where you get the lender's permission to sell the property for less than the loan balance. A deed in lieu is where you turn over the deed to the property to avoid foreclosure. In both cases, you lose your home, but these options may hurt your credit less than foreclosure.

Both of these also require the lender’s permission because they may result in a deficiency. But the lender may agree to them if they believe they’ll be better off doing this rather than foreclosing since foreclosures can be extremely expensive. When you make an agreement with the lender to do either of these you can ask them to forgive the deficiency balance or reduce it. If they agree, get it in writing. If you have to pay something, you may be able to work out an installment payment agreement.

Bankruptcy as a Defense to a Deficiency Lawsuit

You can also get the deficiency balance discharged or eliminated by filing bankruptcy. This works a little differently in Chapter 7 versus Chapter 13 bankruptcies and based on whether you have any non-exempt equity the lender could attach a lien to.

Chapter 7 bankruptcies help eliminate unsecured debts. In most Chapter 7 bankruptcy cases, deficiency judgments are treated as unsecured debt, just like a credit card debt or medical bill. This means the deficiency can be discharged and the lender can’t pursue you for the debt anymore. This is true in most Chapter 7 cases because most filers don’t have any non-exempt equity. Less commonly, the debt can become secured debt after the deficiency judgment is issued. You’ll still be able to eliminate this debt in Chapter 7 to the extent that you don’t have non-exempt equity.

Things get a little more complicated if you have non-exempt equity. In this case, you may want to file Chapter 13 bankruptcy. Unless the lender places a lien on your other assets, the deficiency judgment will be an unsecured debt, dischargeable following your 3-5 year repayment plan. The lender won’t likely receive much through your repayment plan, and once it’s over, the debt is gone.

Working Out a Payment Plan With Your Lender

If you can't defend a deficiency lawsuit, it's time to settle. You’ll want to settle for an amount you can afford to pay because not paying a judgment can damage your credit score. Having a bad credit score means you'll pay more for other loans.

It’s useful to know what you would have to pay if you were to file bankruptcy. If you know you wouldn’t have to pay anything if you filed bankruptcy, you'll have a very strong hand negotiating a very low monthly payment. After all, if they don’t agree, you can file a bankruptcy case, and they’ll miss out on collecting any money at all. If you know you'll have to pay $400 per month in a Chapter 13 bankruptcy, you wouldn't want to agree to pay much more than $400 per month in an installment agreement with the judgment creditor.

Let’s Summarize…

Mortgage companies usually don't sue borrowers for a deficiency after a foreclosure. If they do, understanding your state’s laws can help you stop the mortgage company from suing for a deficiency balance or minimize what you’ll owe. You may only owe the difference between the sale price and your home’s fair market value, rather than what it sold for at the foreclosure sale. You may be able to eliminate the deficiency if the statute of limitations to sue you has passed or if the mortgage company robo-signed documents.

If all else fails, you can file bankruptcy. This is the ultimate debt relief tool to prevent a deficiency judgment against you. A Chapter 7 bankruptcy can eliminate a deficiency balance just as it can eliminate credit card debt. For a simple straightforward Chapter 7 bankruptcy, Upsolve has a free tool you can use to file your bankruptcy without an attorney. For more complicated Chapter 7 bankruptcies or Chapter 13 bankruptcies, Upsolve can help you find an experienced bankruptcy attorney in your area.